Measuring the impact of environmental risk and climate change perceptions

Community views

Contributor

In 2022, the population of NSW is forecast to be one-quarter of a million less than pre-covid forecasts. And yet, as in Victoria, the construction of new housing surges ahead. Are we heading for oversupply, or simply a long-overdue correction?

With the production of our latest forecasts for the regions of New South Wales, one of the most significant findings relates to the Sydney housing market. These forecasts raise the question: is the current level of development is potentially unwarranted with the drop in overseas migration? Could this provide Sydneysiders with the opportunity to enter the housing market with a forecast oversupply of new dwellings in the near future?

The following analysis shares data from our Covid-adjusted Small Area Forecast information (SAFi) product. Learn more about SAFi here, or subscribe to be notified when the latest revision of these forecasts are made available in a region of interest to you.

The demand side

In 2022, the population of New South Wales is forecast to add one-quarter of a million fewer people than forecast prior to the pandemic.

Since Sydney normally receives the bulk (over 80 percent) of NSW’s Net Overseas Migration (NOM), it is not surprising that it is projected that Sydney will be harder hit than Regional NSW by the decline in NOM caused by the closure of Australia’s international borders. In 2022, our Covid-adjusted forecasts show Greater Sydney is expected to be home to 5,150,000 people. Prior to the COVID-19, this was forecast to be 220,000 more people. This shows the magnitude of the impact of the pandemic on the population of our major cities. The vast majority of this decline (196,000 persons) is due to a drop in NOM.

The supply-side

Despite little or no population growth, NSW is currently experiencing high levels of property development and dwelling activity. The NSW Government’s 2021-2022 Intergenerational report suggests that the New South Wales long-term need for additional housing remains, with an expected 1.7 million additional homes by 2061-61.

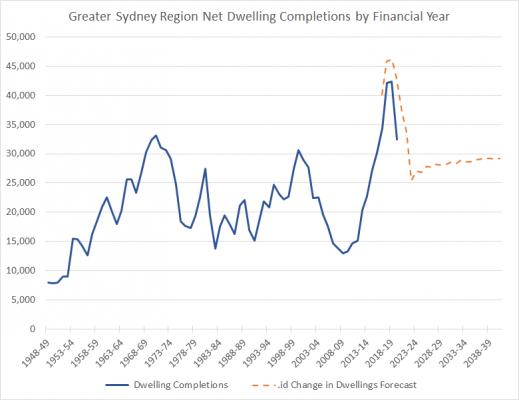

According to the Greater Sydney Regional Housing Activity, from NSW Planning, Industry and Environment, peak construction was occurring in the financial year 18/19 with the 74,000 additional dwellings constructed in NSW. This dropped to 60,000 in financial year 19/20, however, is still a considerable increase of dwelling stock. For Sydney, the new dwellings constructed in FY18/19 was 42,414, and in FY19/20 (the latest data available) this dropped to 31,464 new dwellings. With the downward revision of the forecast population as a result of COVID-19, are these levels of dwelling activity in NSW sustainable?

In crude terms, with a downward revision of 220,000 persons in Sydney in 2022, and assuming an average household size of 2.75, this implies there will be 80,000 fewer households required within the metro area. With the current rate of new housing (approx 40,000 per annum in Sydney), these figures infer that Sydney would not need to build any new dwellings for the next 2 years. Or has COVID-19 and closed borders provided a chance for Sydneysiders to get into the housing market after long-term housing shortages?

Over ten years at the turn of the century, Sydney housing construction slowed to levels not seen since the early 1950’s, resulting in housing shortages. Since 2010, the construction industry has been playing catch up to reach peak levels of new housing experienced today (>40,000 dwellings per annum). With the reduced demand expected in the immediate future, it will be interesting to watch how this plays out in the market, particularly given the cumulative impact of continued closed borders extends the gap between population growth and the supply of dwellings.

Source: Greater Sydney Regional Housing Activity and .id

This supply/demand imbalance could correct in a few ways;

Other possible scenarios that may lead to a minor correction include:

A departure from Economics 101

Economic theory tells us that with a reduction in demand (population), we would expect a corresponding decrease in supply. If excess supply is available, prices of that commodity and production would fall. We also would expect higher vacancy rates, which would then result in a drop in housing prices.

However, in the last 12 months, NSW house prices have continued to rise and although the number of dwelling completions has fallen from historically very high levels, the number of dwellings being constructed in NSW remains historically high.

Many factors influencing housing

Of course, there are other factors besides basic supply and demand that contribute to the current environment. The housing construction industry is an important sector of the economy which governments seek to protect. For example, in 2020, to create consumer demand in the industry, the Commonwealth Government provided eligible applicants grants to build a new home or substantially renovate an existing home.

Further factors in this equation include

Our dwelling forecasts

Our Covid-adjusted forecasts for the regions (SA4s) of New South Wales have the state adding approximately 40,000 dwellings per annum over the long term to its dwelling stock. This requires that the vacancy rate rises to just over 11% before gradually falling over time. We have also assumed a small decline in average household sizes in Sydney and also a decline in the number of younger people living in non-private dwellings (that is, mainly students living in university halls of residence and colleges).

In the longer term, .id is assuming that while net overseas migration to NSW will recover, it will not recover to the levels assumed in the pre-covid world. As Australia’s international borders reopen and net overseas migration returns to more normal levels, it is projected that Sydney will return to positive population growth and that Sydney will grow faster than Regional NSW in both absolute numbers and in growth rates.

Stay tuned for a closer look

We will be unpacking this topic in more detail in an upcoming eBook. Stay tuned for more information and the opportunity to pre-register for your copy. Or, learn more about our Small Area Forecast information (SAFi) or Residential Development Forecasts we have available to help organisations understand the impact of COVID-19 on their catchment, service area or existing strategies or plans.

Photo credit: ©Macourt Media Canva.com

Our specialists have deep expertise in demographics and spatial analysis, urban economics, housing research, social research and population forecasting

Head of Customer and Commercial (Gov.)

Senior Marketing Manager

Demographic Consultant

Client Engagement Manager (WA)

Lead Housing Consultant

Head of Product (Government)

Sales & Account Management (VIC/SA/TAS)

Views Delivery

Forecaster

Customer Success Manager

Customer Success Manager